NVIDIA frenemy relation with OpenAI and Oracle

I’ve spent the last 48 hours completely falling down the rabbit hole of NVIDIA’s Q3 Fiscal 2026 earnings report. If you just skim the headlines, everything looks perfect: Revenue is up 62% to $57 billion, and Jensen Huang is talking about a "virtuous cycle of AI."

But I wanted to understand what was really happening under the hood, so I dug into the balance sheet and cross-referenced it with all the news swirling around OpenAI and Oracle. I’m not a professional Wall Street analyst, but even just connecting the dots myself (with the help of Gemini), I’m seeing some cracks in the "AI Alliance." While NVIDIA posts record numbers, it feels like their biggest customers are quietly arming themselves for a breakout.

Here is my take on the hardware market, the "frenemy" dynamics between OpenAI and NVIDIA, and the "circular financing" theories that everyone—including Michael Burry, has been talking about.

Here is a quick summary of the points I'll discuss below:

- NVIDIA’s Earnings: Perfection with a side of stress

- Making Sense of the Round-Tripping News

- OpenAI making moves to reduce dependency on NVIDIA

- An interesting idea for Oracle: Groq acquisition

- Final Thoughts

NVIDIA’s Earnings: Perfection with a side of stress

On the surface, NVIDIA is the absolute monarch of the AI era. You can’t argue with a Data Center segment that now makes up nearly 90% of the company's business. However, when I looked closer at the financials, I found three specific things that stood out to me as "red flags."

- The Cash Flow Mystery: NVIDIA reported a massive $31.9 billion in Net Income, but when I checked the cash flow statement, they only generated $23.8 billion in Operating Cash Flow. That is an $8 billion gap where profits aren't converting to cash immediately.

- The Inventory Balloon: I noticed that inventory has nearly doubled this year, hitting $19.8 billion. Management says this is to prep for the "Blackwell" launch, but holding ~120 days of inventory seems like a huge capital drag to me.

- The "Paper" Chase: I calculated their Days Sales Outstanding (DSO), and it has crept up to about 53 days. As revenue skyrockets, NVIDIA is waiting nearly two months to get paid, which suggests they might be extending massive credit terms to enterprise clients to keep the flywheel spinning.

My personal read? NVIDIA is "burning the furniture" to build inventory, betting everything that the Blackwell architecture will sell out instantly in Q4.

Making Sense of the Round-Tripping News

I want to be clear: I didn't discover this next part. It’s been all over the financial news lately, and if you follow Michael Burry (the "Big Short" guy), you’ve probably seen his tweets warning about "circular financing" and suspicious revenue recognition.

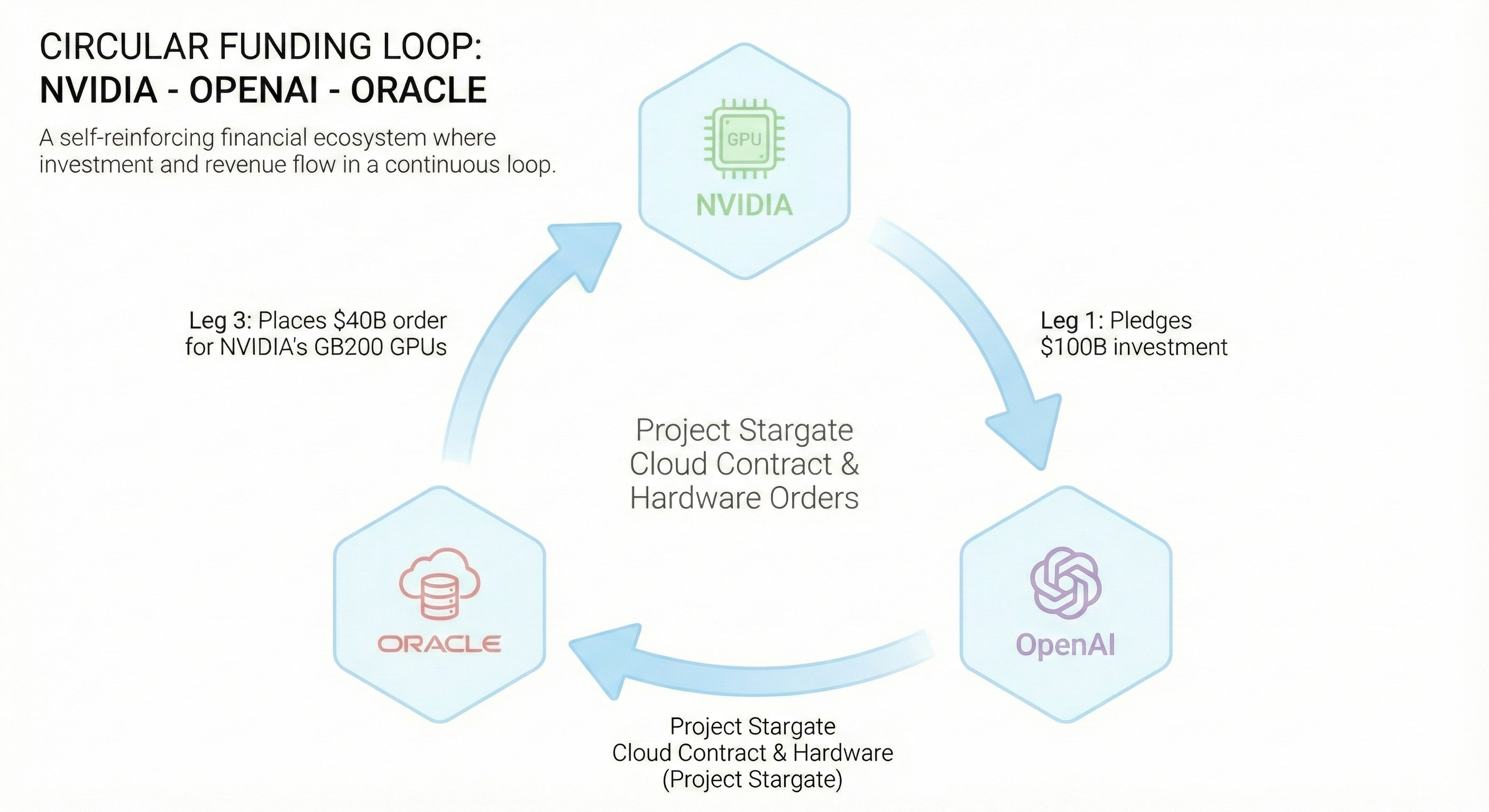

I wanted to map it out for myself to see what the fuss was about. Burry shared a chart recently that visualizes a "web" of deals, and it looks something like this:

- Leg 1: NVIDIA pledges billions (part of a widely reported $100B investment roadmap) to OpenAI.

- Leg 2: OpenAI signs a massive $300 billion cloud contract with Oracle (Project Stargate) to host its models.

- Leg 3: To fulfill that contract, Oracle turns around and places a $40 billion order for NVIDIA’s GB200 GPUs.

Here is the Nano Banana Pro generation I just did for the visual people out there:

Burry’s argument, and the reason regulators like the DOJ are reportedly looking into this—is that this mimics "Round-Tripping." It raises a tough question: If NVIDIA stopped investing in OpenAI, would OpenAI still have the cash to sign that deal with Oracle? And would Oracle still buy those chips? If the answer is "no," then some of that revenue might be more fragile than it looks.

OpenAI making moves to reduce dependency on NVIDIA

The other big shift I’ve been tracking is OpenAI’s pivot. They used to be NVIDIA’s star pupil, but now they look more like a future rival. On one hand, they are hugging NVIDIA tight—deploying 10 gigawatts of infrastructure to train GPT-6. But on the other, they seem to be building a supply chain to kill their dependency on Jensen Huang.

The evidence is pretty loud if you look for it. "Project Stargate" isn't just a data center; it's a huge infrastructure plan that includes custom hardware. OpenAI made some news buying DRAM wafers directly from Samsung and SK Hynix (the 2 main HBM world provider), bypassing NVIDIA’s supply chain, and many others, as reported here, here, or here, and widely debated on Hacker News here.

Plus, the talent migration is telling: OpenAI has poached key silicon talent, including Richard Ho (Google’s former TPU lead) back in 2023, and more recently many hardware engineers from Apple (around 40 apparently).

With the Broadcom partnership, my guess is OpenAI plans to use NVIDIA GPUs to create intelligence, but run that intelligence on their own custom silicon to stop bleeding cash, or by betting on Edge TPU-like chips for inference, similar to what Google does with its NPU chip.

The big question is, which money is Openai planning on using to fund this? and how much influence does NVIDIA has over OpenAI’s future plans?

The $100 billions that NVIDIA is "investing" in OpenAI is not yet confirmed neither, as reported here,

An interesting idea for Oracle: Groq acquisition

Everyone is talking about Inference costs right now, basically, how expensive it is to actually run ChatGPT or any other LLMs versus training it. Now I'm looking at Groq, a startup claiming specifically to be faster and cheaper than NVIDIA for this task. The founder is Jonathan Ross, a former Google TPU lead and literally the person that basically had the idea of TPU.

There is another layer to this that I think is getting overlooked as well: The HBM Shortage created by Openai’s direct wafer purchases.

From what I understand, one of the biggest bottlenecks for NVIDIA right now is HBM (High Bandwidth Memory), which is manufactured in specialized memory fabs that are completely overwhelmed. However, Groq’s architecture relies on SRAM (Static RAM). Since SRAM is typically built in logic fabs (like TSMC) alongside the processors themselves, it theoretically shouldn't face the same supply chain crunch as HBM.

Looking at all those pieces, I feel Oracle should seriously look into buying Groq. Buying Groq wouldn't just give Oracle a faster chip, it could give them a chip that is actually available when everything else is sold out. It’s a supply chain hedge.

It's also a massive edge for its main client, OpenAI, to get faster and cheaper inference.

Combine that with the fact that Oracle’s margins on renting NVIDIA chips are brutal, reportedly as low as 14%, then the deal just makes sense. By owning Groq, Oracle could stop paying the "NVIDIA Tax," fix their margins, and bypass the HBM shortage entirely.

Groq currently has a valuation of around $6.9 billions, according to its last funding round in september 2025. Even with a premium, Oracle has financial firepower to make that acquisition happen.

But would NVIDIA let that happen? and if the answer is no, then what does that tell us about the circular funding in place? Is there a Quid pro quo where Nvidia agrees to invest 100 billions in OpenAI in exchange of Oracle being exclusive to Nvidia?

Final Thoughts

As we head into 2026, when looking at Nvidia, openai and Oracle dynamics, it looks like they are squeezing each other balls. I do not know if Nvidia knew about the Openai deal about the wafer memory supply, or was there any collusion? Does NVIDIA is fighting to maintain exclusivity for both training and inference at Stargate? What kind of chips is Openai planning on building ? TPU/LPU like? Or more Edge TPU?

Michael Burry is betting against the whole thing.

Me, I’m just a guy reading the reports, I have no way to speculate on this market. But I do know one thing: The AI hardware market is hotter than ever, and the next few quarters are going to be fascinating to watch.

I have not discussed much about TPU from Google in this article, but I cover some thoughts about the TPU vs GPU in a previous post recently.. It seems Google responded quickly to the current situation about the memory wafer shortage by securing a major deal with Samsung in 2026.

Disclaimer: I say very smart things sometimes, but say stupid things a lot more. Take this in consideration when reading this blog post